SIP → SWP Playbook

SIP Calculator with Inflation to SWP Guide (Step-Up Ready)

Learn how to grow your SIP with inflation awareness, add a step-up, and convert the corpus into a tax-aware SWP. Includes a worked example, comparison table, and direct links to our SIP, step-up SIP, and SWP calculators.

Inflation-adjusted SIP now, smoother SWP later

A SIP that ignores inflation looks great on paper but disappoints at withdrawal time. Pairing an inflation-aware SIP with a planned SWP reduces sequence-of-returns risk and keeps your monthly income predictable.

Example assumption (not advice): 10% expected equity returns, 6% inflation, 10% annual step-up, and a 3.8% SWP withdrawal rate. Adjust these in the calculators to fit your goals.

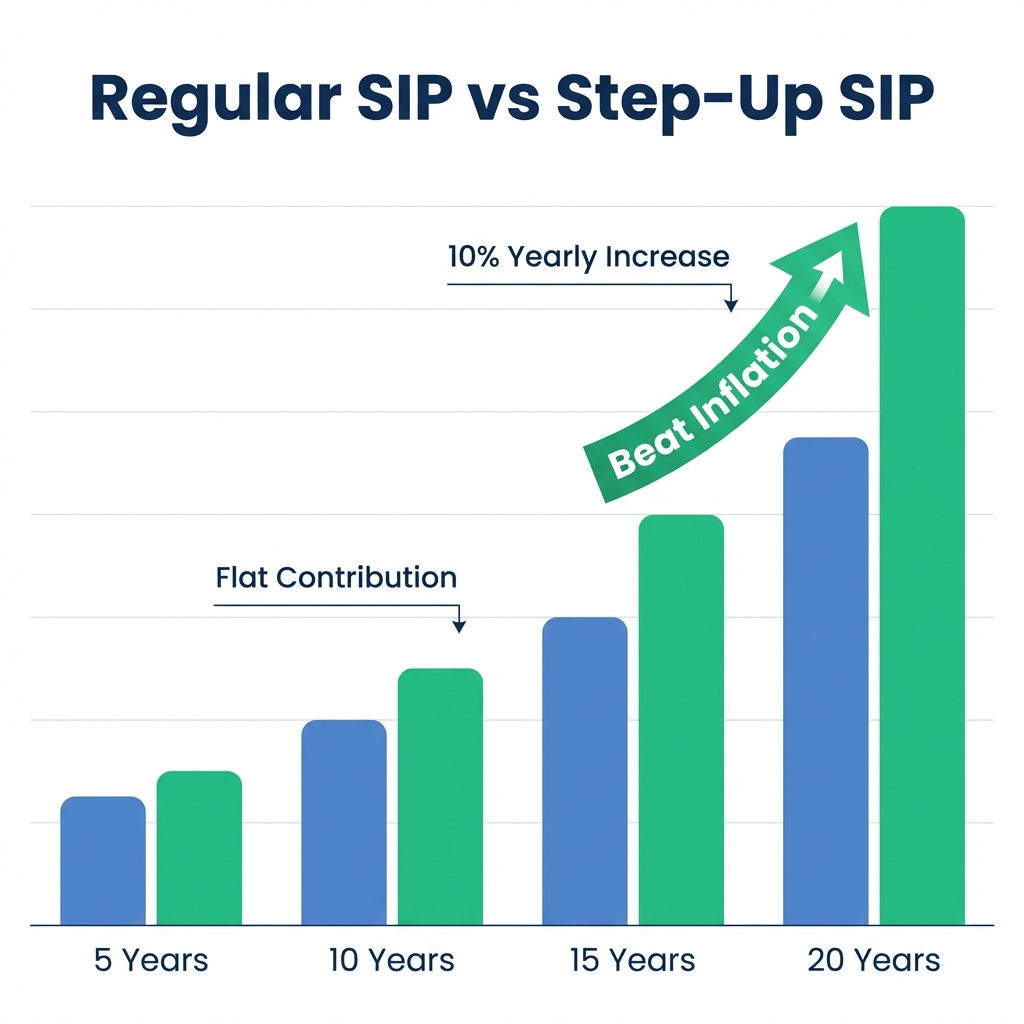

Regular vs Step-Up SIP vs SWP (Worked Snapshot)

Scenario: ₹10,000 monthly SIP, 20 years, 12% nominal return, 6% inflation. Step-up SIP increases the contribution by 10% each year. SWP uses a 3.8% annual withdrawal rate post-retirement.

| Plan | Contribution Pattern | Projected Corpus (Nominal) | Inflation-Adjusted Corpus | Notes |

|---|---|---|---|---|

| Regular SIP | ₹10,000/month, no increase | ~₹99 lakh | ~₹31–32 lakh | Good for consistency; may lag inflation-heavy goals. |

| Step-Up SIP | ₹10,000/month with 10% yearly bump | ~₹1.53 crore | ~₹47.7 lakh | Tracks salary growth; builds a stronger real corpus. |

| SWP Phase | 3.8% annual withdrawal, inflation-linked | ~₹48,500/month starting payout | Purchasing power preserved if returns stay ahead of inflation | Rebalance yearly; keep 12–18 months of SWP in debt/liquid. |

These numbers are illustrative, rounded, and assume steady returns. Markets, taxes, and inflation will vary. Always test your own inputs in the calculators.

Step-Up SIP vs Regular SIP: Why the bump matters

A 10% annual step-up can lift your real corpus by 40–60% compared to a flat SIP, because contributions grow alongside your income while inflation erodes flat contributions.

Step-up SIP meaning: it is an automatic step up SIP instruction that raises your SIP each year, matching salary growth without manual edits.

Quick comparison

- Flat SIP: ₹10,000 × 240 months ≈ ₹24 lakh contributed → ~₹99 lakh nominal corpus.

- Step-up SIP (10% yearly): Contributions rise from ₹10,000 to ~₹61,000/month by year 20 (₹10,000 × 1.10¹⁹) → ~₹1.53 crore nominal corpus.

- Inflation gap: At 6% inflation, the step-up keeps pace with lifestyle creep and tuition/healthcare costs better than a flat SIP.

Use the step up SIP calculator based on salary to test 5%, 8%, and 10% increments, then compare the inflation-adjusted corpus.

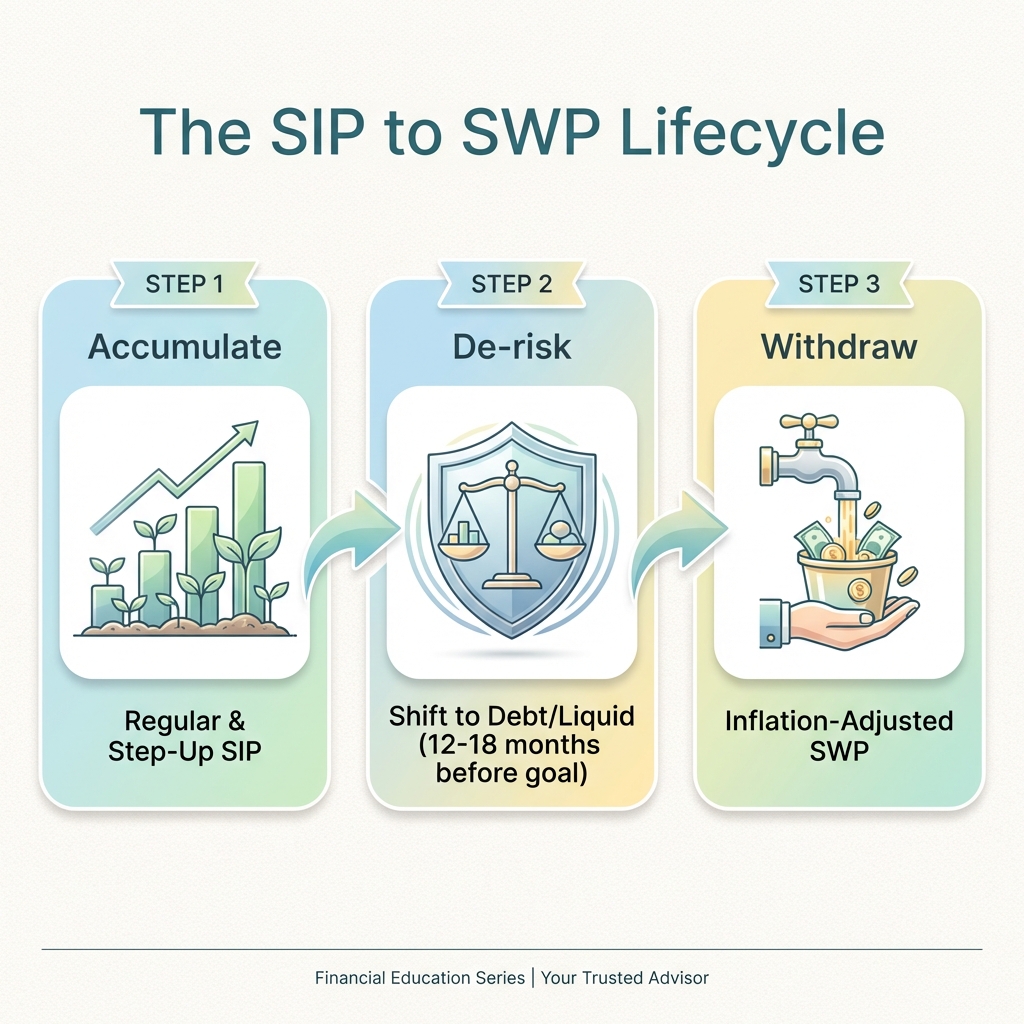

SIP → SWP lifecycle: Accumulate, de-risk, withdraw

- Accumulate: Build with a SIP calculator (preferably inflation-aware). Add a small debt allocation for stability.

- Accelerate: Shift to a step-up SIP once salary hikes start.

- De-risk: 12–18 months before retirement, move 2–3 years of expenses to debt/liquid; keep the rest diversified.

- Withdraw: Use the SWP calculator with inflation to set a withdrawal rate (e.g., 3.5–4.0%) and test longevity.

- Review annually: Rebalance, refresh inflation assumptions, and re-run SIP vs SWP scenarios.

A SIP to SWP ladder splits the corpus by time horizon so near-term withdrawals are protected from equity volatility. That's a simple systematic withdrawal plan example you can tweak for retirement goals.

How to use our calculators (quick tour)

SIP Calculator

Enter monthly SIP, expected return, and inflation to see real maturity values. The mutual fund SIP return calculator includes a "how to use SIP calculator" helper inside the tool.

Open SIP calculator →Step-Up SIP

Model 5–15% annual increments to match salary growth and close inflation gaps.

Try step-up SIP →SWP Calculator

Set a withdrawal rate, add inflation, and view how long the corpus can last.

Plan SWP payouts →Decision checklist

Confirm an inflation assumption (e.g., 6%) and test higher private inflation (education/healthcare at 8–10%).

Pick a step-up rate aligned with your salary hikes (5–10% typical). Adjust if bonuses are uneven.

Set a SWP withdrawal rate and run downside scenarios. Keep 12–18 months of SWP in low-volatility funds.

Review taxes annually. Equity SWP redemptions can trigger LTCG/STCG; debt funds have different tax rules.

Calculation Methodology & Verification

How we calculated the numbers:

Regular SIP (₹10,000/month, 12% annual return, 20 years):

- Formula: FV = PMT × [(1+r)ⁿ - 1] / r, where r = 0.01 (1% monthly), n = 240 months

- Nominal corpus = ₹10,000 × [(1.01)²⁴⁰ - 1] / 0.01 = ₹99.91 lakh

- Inflation adjustment: ₹99.91 lakh / (1.06)²⁰ = ₹99.91 / 3.207 = ₹31.15 lakh (real value)

Step-Up SIP (₹10,000 start, 10% annual step-up, 12% return, 20 years):

- Year 1 contribution: ₹10,000/month; Year 20: ₹10,000 × (1.10)¹⁹ = ₹61,159/month

- Each year's SIP grows separately: Year-1 SIP compounds for 20 years, Year-2 for 19 years, etc.

- Approximate total corpus (sum of all yearly cohorts): ~₹1.53 crore nominal

- Inflation-adjusted: ₹1.53 crore / 3.207 = ₹47.7 lakh (real value)

SWP Phase (3.8% annual withdrawal):

- Starting withdrawal from ₹1.53 crore: ₹1.53 crore × 0.038 = ₹5.814 lakh/year

- Monthly payout: ₹5.814 lakh / 12 = ₹48,450/month (~₹48,500)

- With 6% inflation indexing, payout rises annually to maintain purchasing power

Important: Calculations assume constant returns for simplicity. Real markets fluctuate, and sequence-of-returns risk can significantly impact SWP sustainability.

Inflation is user-controlled; private inflation (education/healthcare) can be 8-10%, higher than CPI.

Disclaimer: We are not SEBI registered investment advisors. This content is for educational purposes only. Please consult a qualified financial advisor before making investment decisions.

SWP longevity depends on actual returns, asset allocation, rebalancing discipline, and tax efficiency.

FAQs

How does a SIP calculator with inflation help me plan real returns?

It adjusts your SIP projections for expected inflation so you see both nominal and real (purchasing power) values. A mutual fund SIP return calculator with inflation shows if your corpus will beat rising costs, and the help text inside explains how to use the SIP calculator inputs correctly.

When should I switch from SIP to SWP?

Switch after you have a target corpus and a withdrawal plan. A common pattern is 12–18 months before withdrawals: pause equity top-ups, move part of the corpus to debt, and then start an inflation-linked SWP.

What is the difference between SIP and SWP?

SIP is a Systematic Investment Plan (money goes in), while SWP is a Systematic Withdrawal Plan (money comes out). SIP builds the corpus; SWP converts it into monthly cash flow.

How do I use a step up SIP calculator?

Enter your starting SIP, choose an annual step-up (for example 10%), and set expected returns plus inflation. The calculator shows how progressive contributions accelerate corpus growth versus a flat SIP.

What is a good SWP withdrawal rate in India?

A conservative starting point is 3.5%–4.0% annualized, adjusted for inflation. Always test in the SWP calculator with inflation so you see how long the corpus lasts under different return and withdrawal assumptions.

How is SWP taxed compared to SIP redemptions?

Each SWP installment is treated like a partial redemption: equity funds apply LTCG/STCG rules based on holding period of the units sold. Check the SWP calculator with tax notes and consult a tax advisor for personalized guidance.

What is a SIP to SWP ladder?

It staggers redemptions: near-term SWP needs sit in debt/liquid funds, medium-term in balanced funds, and long-term in equity. This reduces sequence-of-returns risk when withdrawals begin.

How do I calculate SIP maturity amount with step-up?

Use the step up SIP calculator, input your starting SIP, annual increment, tenure, expected return, and inflation. It computes both nominal maturity and inflation-adjusted maturity.

What is SIP and SWP meaning for retirement income?

SIP (Systematic Investment Plan) is how you build the corpus, and SWP (Systematic Withdrawal Plan) is how you draw from it for retirement income. A SIP vs SWP difference is money-in versus money-out; both should be modeled together so SWP for retirement income lasts through market cycles.