EPF Scheme 2026: New PF Withdrawal Rules Explained

The Employees' Provident Fund Scheme, 1952 has been replaced with effect from 29 June 2026. Here's exactly what changes for partial and full PF withdrawal.

Calculate Your EPF Balance →25%

Minimum Balance

Must always remain in your account

12 mo.

Uniform Eligibility

Same wait for every partial withdrawal category

12 mo.

Unemployment Wait

For full withdrawal (was 2 months earlier)

EPF Scheme 2026 withdrawal rules at a glance — full text breakdown below.

Latest EPF Withdrawal Claim Rules

Notified 29 June 2026 · Employees' Provident Fund Scheme, 2026

Essential Needs

Withdrawals for illness, education, and marriage of self or family.

Housing Needs

Purchasing or constructing a house, a plot, or repaying a home loan.

Special Circumstances

Events such as unemployment or natural calamity — no reason needs to be stated.

- Minimum service period

- Uniformly reduced to just 12 months of membership for all partial withdrawals.

- Calculation basis

- Based on both the employee's and the employer's share (plus interest).

- Withdrawal limit

- Up to 75% of your total balance for these purposes — i.e. 100% of your Eligible Member Balance, since the 25% Minimum Balance must remain.

- Withdrawal frequency

- • Education: up to 10 times

- • Marriage: up to 5 times

- • Housing: up to 5 times during membership

- • Special circumstances: up to 2 times per financial year

- Unemployment / premature settlement

- Up to 75% of your PF can be withdrawn; the remaining 25% is available after 12 months of continuous unemployment.

- EPS (pension) withdrawal

- Governed by the separate Employees' Pension Scheme, 2026. A withdrawal benefit is not available once you complete 10 years of eligible service — you receive a monthly pension instead. Confirm the current waiting period with EPFO.

- Full withdrawal (entire balance)

- Withdrawal of the entire PF balance (including the 25% Minimum Balance) is permitted on: retirement after age 55, permanent and total incapacity to work, voluntary retirement (VRS), retrenchment, or permanent migration abroad.

Automated Withdrawal Process

Partial withdrawals are moving to a largely paperless, automated settlement — under the new digital-first framework, supporting documentary proof is generally not required for a partial withdrawal claim.

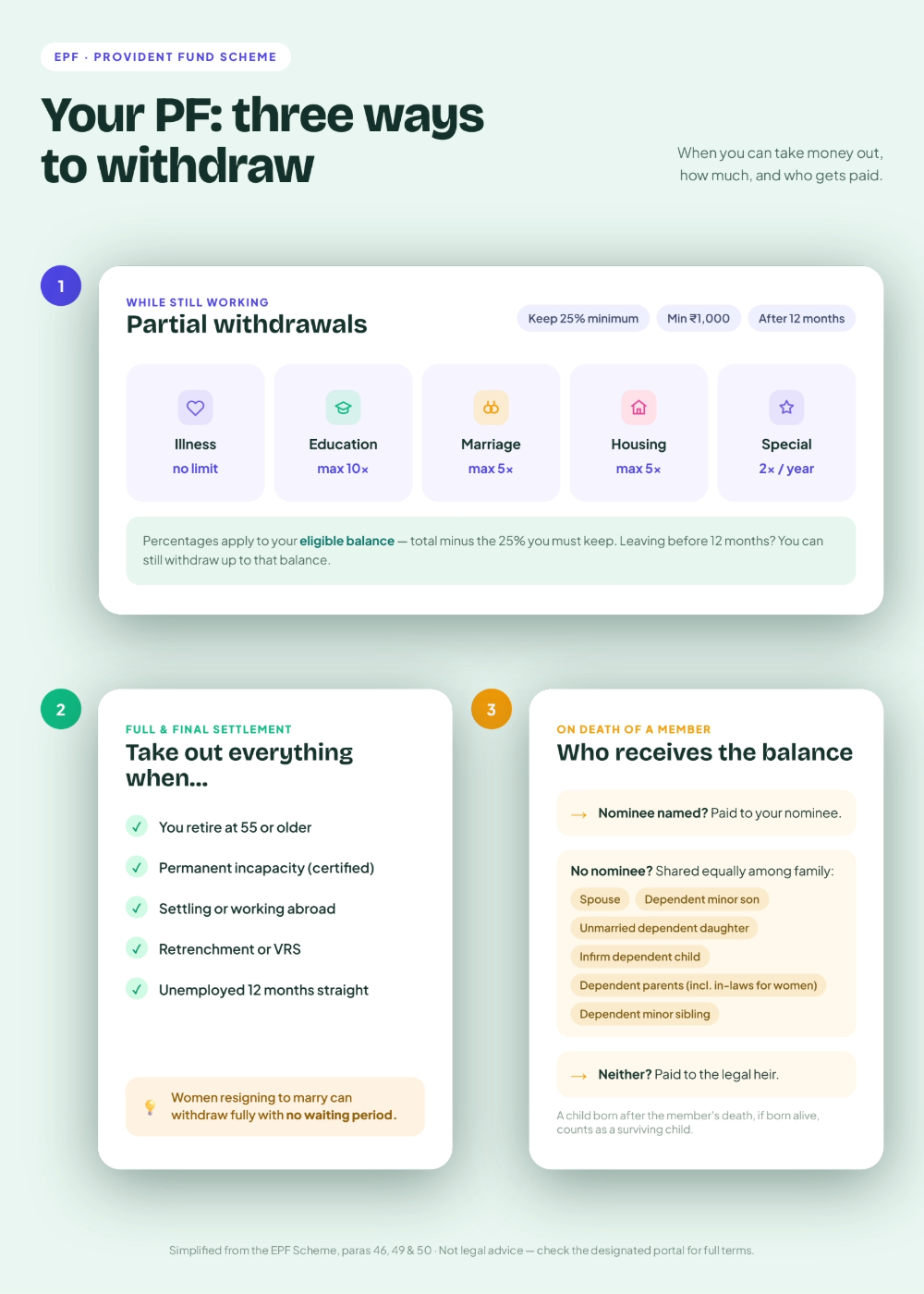

Summary of the Employees' Provident Fund Scheme, 2026 (Paragraphs 46–49). Percentages are of your total accumulated PF corpus (employee + employer share + interest).

What Is the EPF Scheme, 2026?

On 29 June 2026, the Ministry of Labour & Employment notified the Employees' Provident Fund Scheme, 2026, published in the Gazette of India, Extraordinary, Part II — Section 3(i). It is made under the powers granted by the Code on Social Security, 2020 — one of the four labour codes that came into force on 21 November 2025 — and it supersedes the Employees' Provident Fund Scheme, 1952 with immediate effect.

Every person who was a member (or was required to be a member) of the EPF Scheme, 1952 up to the date it ceased to apply automatically continues as a member of the new 2026 Scheme — there is no fresh enrolment required for existing members. Alongside it, the government also notified the Employees' Pension Scheme, 2026 and the Employees' Deposit Linked Insurance Scheme, 2026.

Employer and employee contribution rates are unchanged — both remain capped at 12% of wages. The overhaul is concentrated in how and when you can withdraw your PF balance, plus tighter digital-compliance and claim-processing rules.

The New Core Concept: Minimum Balance & Eligible Member Balance

Every partial withdrawal calculation under EPF Scheme 2026 now runs through two defined terms (Paragraph 46):

Minimum Balance

25% of your aggregate total contributions (employee's share + employer's share + interest earned on both, up to the date of withdrawal) that must remain in your account after any partial withdrawal.

Eligible Member Balance (EMB)

Your total balance minus the Minimum Balance. This is the maximum amount from which a partial withdrawal (up to 100%) can be sanctioned.

Example: if your total PF balance is ₹4,00,000, your Minimum Balance is ₹1,00,000 (25%) and your Eligible Member Balance is ₹3,00,000 — up to all of which can be withdrawn for an approved purpose, subject to the frequency caps below. The minimum amount for any partial withdrawal is ₹1,000.

Partial Withdrawal: 3 Categories, 5 Purposes (Paragraph 46)

The old scheme's roughly 13 separate withdrawal grounds are consolidated into 3 categories — essential needs (illness, education, marriage), housing, and special circumstances — covering 5 distinct purposes. All require 12 months of total Fund membership, except members exiting service before 12 months (see note below).

| Purpose | Min. Membership | Withdrawal Limit | Frequency Cap |

|---|---|---|---|

| Illness (self / family) | 12 months | Up to 100% of Eligible Member Balance | Not capped |

| Education (self / family) | 12 months | Up to 100% of Eligible Member Balance | Max 10 times |

| Marriage (self / family) | 12 months | Up to 100% of Eligible Member Balance | Max 5 times |

| Housing (purchase, site, construction, home loan repayment, renovation) | 12 months | Up to 100% of Eligible Member Balance | Max 5 times |

| Special circumstances (general purpose) | 12 months | Up to 100% of Eligible Member Balance | Max 2 times per financial year |

Exiting before 12 months? A member who leaves service before completing 12 months of Fund membership is still eligible for partial withdrawal, capped at the Eligible Member Balance on the date of exit — the usual 12-month wait does not apply in this case.

Source: Employees' Provident Fund Scheme, 2026, Paragraph 46 (Partial withdrawals from Fund).

What Counts Towards the 12-Month Membership?

Per Paragraph 47, the following periods add up towards the 12-month eligibility threshold for partial withdrawal:

- Total service with the same employer before this Scheme applied to the establishment (excluding breaks)

- Periods of membership of the Fund itself

- Periods of membership of a private provident fund in an exempted establishment

- Periods of membership as an employee exempted under Section 143 of the Code, immediately preceding current membership

This continuity is broken if you previously withdrew (severed membership of) your provident fund during that period — which is another reason transferring your PF via Form 13 when changing jobs is usually better than withdrawing.

Full & Final Withdrawal: What Changed (Paragraph 49)

You can still withdraw 100% of your PF balance on any of these events, largely unchanged from the earlier scheme:

- Retirement after attaining 55 years of age (if you leave service before 55 but turn 55 before your payment is authorised, you remain eligible)

- Retirement due to permanent and total incapacity for work, medically certified

- Immediately before permanent migration from India, or for taking up employment abroad

- Termination due to mass or individual retrenchment

- Termination under a mutual voluntary retirement scheme (VRS)

- Certain establishment closure/transfer scenarios, with actual payment only after a continuous 2-month wait from the date of application

The big change: general unemployment now needs a 12-month wait, not 2 months

For any other case of leaving a Code-covered establishment, the Commissioner may permit full withdrawal only if you have not been employed in any Code-covered establishment for a continuous period of at least 12 months immediately before your withdrawal application. Under the EPF Scheme, 1952, this waiting period was 2 months. The only stated exception is a female member resigning from service for the purpose of getting married, for whom no waiting period applies.

If you take up employment again after such a full withdrawal, you are treated as a fresh member and must requalify for Fund membership — service continuity is not preserved.

In practice, this means members who lose or leave a job now have to rely more heavily on the "special circumstances" partial withdrawal (up to 100% of Eligible Member Balance, twice a financial year) for near-term liquidity, since full account closure takes a full year of continuous unemployment.

Claim Filing & Settlement Timelines (Paragraph 54)

- Claims are filed on the designated EPFO portal at the time of leaving service, as before

- If online filing isn't possible for technical reasons, a physical claim can still be forwarded through your employer, who must verify, attest, and forward it within 5 days of receipt

- Payment is made via electronic/digital transfer to a Scheduled Bank, Co-operative Bank (including Urban Co-operative Banks), or post office account

- Claims complete in all respects must be settled and paid within 20 days of receipt by the Commissioner

- Any deficiency in a claim must be communicated to the claimant within 20 days

- If the Commissioner fails, without sufficient cause, to settle a complete claim within 20 days, penal interest at 12% per annum on the benefit amount becomes chargeable

EPF Scheme 1952 vs EPF Scheme 2026: Side by Side

| Factor | EPF Scheme, 1952 | EPF Scheme, 2026 |

|---|---|---|

| Number of withdrawal grounds | ~13 separate grounds (Paras 68B–68N), each with its own conditions | 5 consolidated categories: illness, education, marriage, housing, special circumstances |

| Minimum service required | Varied by purpose — 5, 7 or 10 years depending on the ground | Uniform 12 months of total Fund membership for all categories |

| Withdrawal limit basis | Multiples of monthly wages (Basic + DA), e.g. 24–36 months' wages | Up to 100% of the Eligible Member Balance (balance after the 25% Minimum Balance) |

| Minimum balance retention | Not a standalone rule | 25% of aggregate contributions (employee + employer + interest) must remain after any partial withdrawal |

| Full withdrawal after leaving job | Full balance after just 2 months of continuous unemployment | Full balance only after 12 months of continuous unemployment (no exception except female members resigning to marry) |

| Minimum withdrawal amount | No explicit floor in most provisions | Not less than ₹1,000 |

| Claim settlement timeline | Settlement targeted within 20 days (departmental practice) | 20-day settlement is now a statutory requirement (Para 54), with 12% p.a. penal interest on unjustified delay |

What Hasn't Changed

- Contribution rate: 12% of wages each from employer and employee

- Retirement full-withdrawal age: 55 years

- Income-tax treatment: the 5-year continuous service rule for tax-free withdrawal and TDS under Section 192A of the Income Tax Act are separate provisions, unaffected by this Scheme — see our EPF Withdrawal Rules & Tax Guide.

- Nomination, transfer between employers (Form 13-equivalent), and death benefit provisions continue with largely similar structure, now under the Code on Social Security framework

We could not confirm whether a distinct pre-retirement advance provision (previously available from age 54) has been retained as a separate category — near-retirement liquidity needs may now fall under the general "special circumstances" partial withdrawal. Confirm this specific point with your EPFO regional office or the official circular before planning around it.

Calculate Your EPF Balance & Eligible Member Balance

Model your PF corpus and see how much would be available as your Eligible Member Balance under the new 25% Minimum Balance rule.

Open EPF CalculatorFrequently Asked Questions

What is the EPF Scheme, 2026?

The Employees' Provident Fund Scheme, 2026 is a new scheme notified by the Ministry of Labour & Employment on 29 June 2026, under the Code on Social Security, 2020. It supersedes the Employees' Provident Fund Scheme, 1952, with effect from the date of notification. Every existing member of the 1952 Scheme automatically continues as a member of the new Scheme.

What is the biggest change in EPF Scheme 2026?

The biggest change is to partial withdrawals: the old scheme's roughly 13 separate withdrawal grounds (each with its own minimum service requirement of 5, 7 or 10 years) are consolidated into 5 categories — illness, education, marriage, housing, and special circumstances — all requiring just 12 months of Fund membership. A new 'Minimum Balance' rule also requires 25% of your total accumulated contributions to always remain in the account.

What is the Minimum Balance and Eligible Member Balance under EPF Scheme 2026?

Minimum Balance is 25% of your aggregate PF contributions (employee + employer share, plus interest) that must remain in your account after any partial withdrawal. Eligible Member Balance (EMB) is your balance after deducting this Minimum Balance — it is the maximum amount available for partial withdrawal. For example, on a ₹4 lakh balance, the Minimum Balance is ₹1 lakh and the Eligible Member Balance is ₹3 lakh (up to 100% of which can be withdrawn for an approved purpose).

How many times can I withdraw EPF for education, marriage or housing under the new rules?

Under EPF Scheme 2026, partial withdrawal for education (self or family) is capped at 10 times during your entire membership, marriage (self or family) at 5 times, and housing-related withdrawals (purchase, construction, home loan repayment, renovation) at 5 times. Withdrawal for illness has no stated frequency cap. 'Special circumstances' withdrawals are capped at 2 times per financial year. All require 12 months of Fund membership, except members exiting service before completing 12 months, who can still withdraw up to their Eligible Member Balance.

Is the 2-month unemployment withdrawal rule still valid?

No — this is a major change. Under the EPF Scheme, 1952, members could withdraw the full balance after just 2 months of continuous unemployment. Under EPF Scheme 2026, full and final withdrawal on general cessation of employment (paragraph 49(2)) is permitted only after a continuous period of at least 12 months of not being employed in any Code-covered establishment. The only exception is female members resigning to get married, who face no waiting period. Members can still access liquidity earlier through the 'special circumstances' partial withdrawal category, subject to the 25% Minimum Balance rule.

At what age can I withdraw my full EPF under the new scheme?

You can withdraw 100% of your EPF balance on retirement after attaining 55 years of age — this is unchanged from the earlier scheme. If you leave service before turning 55 but reach 55 before your claim is processed, you remain eligible for full withdrawal.

Does EPF Scheme 2026 change the minimum withdrawal amount?

Yes, the new scheme sets a floor: partial withdrawals must be for an amount not less than ₹1,000.

How long does EPFO have to settle a claim under the new scheme?

Paragraph 54 of EPF Scheme 2026 requires claims that are complete in all respects to be settled and paid within 20 days of receipt. Any deficiency in the claim must be communicated to the claimant within 20 days. If the Commissioner fails to settle a complete claim within 20 days without sufficient cause, penal interest at 12% per annum on the benefit amount becomes chargeable.

Do I need to file a fresh claim, or does anything change in how I apply?

The claims process itself is largely unchanged — you file on the EPFO member portal at the time of leaving service (or your employer/nominees file on your behalf in case of death). If online filing isn't possible for technical reasons, you can still submit a physical claim through your employer, who must forward it within 5 days of receipt.

Does the EPF Scheme 2026 change TDS or the 5-year tax-free rule on withdrawal?

No. EPF Scheme 2026 restructures withdrawal eligibility and limits under the Code on Social Security, but the income-tax treatment of PF withdrawals — the 5-year continuous service rule for tax-free withdrawal and TDS under Section 192A — is governed separately by the Income Tax Act and is not altered by this notification. See our EPF Withdrawal Rules guide for the tax rules.

Related Calculators & Guides

Free Calculator

EPF Calculator — FY-wise Rates, VPF & Withdrawal Impact →

Model your EPF corpus with partial withdrawal simulation.

- EPF Withdrawal Rules & Tax Guide — 5-year tax rule, TDS, Form 15G, and the withdrawal process

- EPF TDS Calculator & Form 15G Guide

- New Labour Codes 2026 — Wage Code & 50% Basic Salary Rule

- Is EPF Withdrawal Taxable?

- EPF Interest Rate 2026-27

- EPS Pension Calculator

Sources & References

- Employees' Provident Fund Scheme, 2026 — Gazette of India, Extraordinary, Part II, Section 3(i), notified by the Ministry of Labour & Employment on 29 June 2026 (Paragraphs 43–55).

- EPFO Official Portal — epfindia.gov.in

- e-Gazette of India — egazette.gov.in

Disclaimer

This page summarises the Employees' Provident Fund Scheme, 2026 as notified on 29 June 2026, based on the published Gazette text and contemporaneous reporting. As a newly notified scheme, EPFO circulars, portal changes, and clarifications may follow. Always verify current requirements with your employer's HR department or the EPFO helpdesk before initiating a withdrawal. This website is not affiliated with EPFO or the Government of India.